Image by: Prykhodov, ©2015 Getty Images

Apple and Google have created an infrastructure to facilitate mobile payments and the organization of the many loyalty cards we all have. Both companies are enhancing their versions of the mobile wallet and rebranding them. Apple’s Passbook has been rebranded and is now Apple Wallet, as of iOS 9 and will remain a native app. Google has changed their Google Wallet to become a “peer to peer" payment system. Google has created Android Pay, which is now a true mobile wallet and has become a native app. When I say “native,” I mean that both of these wallets are built right into the phone’s operating systems. Along with the rebranding, you can expect to see increased efforts by both companies to expand customer use of their mobile wallets.

So, what does this mean to the business billers?

When we consider customer responses to traditional e-billing, three of the major customer objections to making the switch from paper to e-billing are:

- Password fatigue: Having to remember too many different usernames and passwords is a hassle and a major inconvenience.

- Extra work for the recipient: Receiving paper is simple—you just wait for the bill to arrive in the mail. Having to log onto a website every month just to retrieve your bill is a nonstarter for many people.

- Paper reminder: Many consumers use the paper as a reminder that they have a bill to pay. With email, too often, it falls off the screen and you forget about it. Unless you act right away, there is a chance that next month you will find yourself with a past due notice with interest and penalties for late payment. Does this sound familiar?

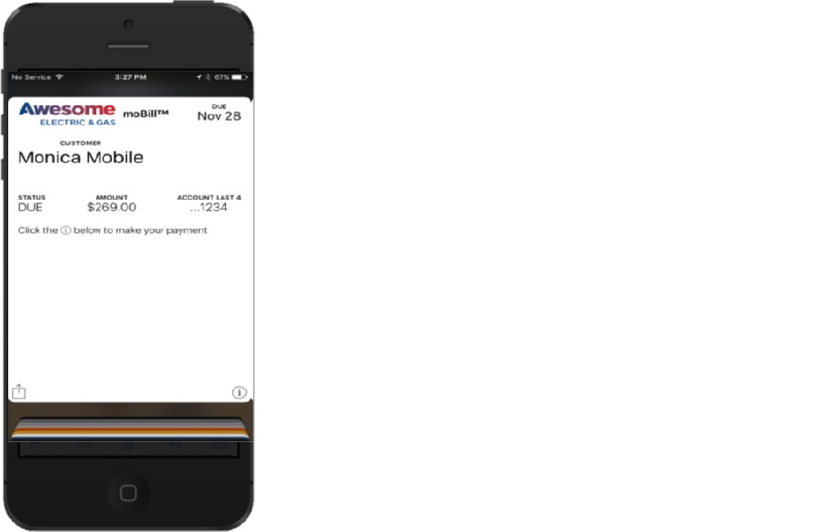

No more password fatigue: Because everything has been pre-authenticated, clients can view their bill in the wallet (including a PDF copy) and pay from the phone, without entering a username, password or account number.

No extra work for the recipient: Bills are automatically downloaded and displayed on the phone. There is no need to log onto a website to retrieve a bill.

The effective use of the Apple Wallet and Android Pay can have a profound effect on how individuals interact with their vendors. As people spend more and more time on their mobile devices and use mobile wallets for everyday activities, it will become more and more important to get positioned, front and center, “in your customer’s wallet.”

Richard Rosen is the chief executive officer of The RH Rosen Group, a firm that provides solutions to help businesses improve processes and customer communications with the intent to create real, recurring benefits in: cost reduction, electronic payment, shipment tracking and printing/mailing. Contact him at RichR@RHRosenGroup.com or visit www.rhrosengroup.com.